In a world where unforeseen circumstances can disrupt your life, disability insurance emerges as a crucial financial safeguard. This article will delve into the depths of disability insurance, answering the ever-present question: “Is disability insurance worth it?”

Reading time: 28 minutes

Outline

- Understanding Disability Insurance

- The Importance of Disability Coverage

- Deciding Whether You Need Coverage

- How to Choose the Right Disability Insurance

- How Much Disability Insurance You Need?

- Where to Buy Disability Insurance?

- The Cost of Disability Insurance

- Filing a Disability Insurance Claim

- Disability Insurance Myths Debunked

- Conclusion

- FAQs

- Case Study

- Checklist

1. Understanding Disability Insurance

Disability insurance, often overlooked, is a critical financial safeguard. It provides income replacement if you become disabled and cannot work, ensuring that you don’t suffer financially during challenging times. Let’s dive deeper into this essential coverage.

1-1. What is Disability Insurance?

Disability insurance is a contract between you and an insurance company. It guarantees a portion of your income if you are unable to work due to an injury or illness. This income replacement comes in the form of regular payments, usually a percentage of your salary. The goal is simple: to help you maintain your standard of living and cover essential expenses when you can’t earn a paycheck.

1-2. The Two Main Types

Disability insurance comes in two primary forms: short-term disability (STD) and long-term disability (LTD) coverage. Each serves a unique purpose, and understanding the differences is crucial for tailoring your protection to your specific needs.

1-2-1. Short-Term Disability (STD) Insurance

Short-term disability insurance provides benefits for a limited duration, typically from a few weeks to a few months. It kicks in quickly, usually within a week or two after the disability occurs. This type of coverage is ideal for temporary disabilities resulting from injuries, surgeries, or illnesses with a shorter recovery period.

Benefits from STD insurance can replace a significant portion of your income during your recovery. It ensures you can continue meeting immediate financial obligations like mortgage or rent payments, utility bills, and groceries.

1-2-2. Long-Term Disability (LTD) Insurance

On the other hand, long-term disability insurance offers protection for more extended periods, often up to several years or until retirement age, depending on the policy. The waiting period before benefits begin is longer than with STD insurance, typically ranging from 30 to 180 days.

LTD insurance is designed for more severe and long-lasting disabilities, such as chronic illnesses or injuries that require extended recovery time. It provides a safety net for your financial well-being when you are unable to work for an extended period.

1-3. Tailoring Your Protection

Understanding the types of disability insurance allows you to tailor your coverage to your specific needs. Consider the following factors when choosing the right policy:

- Your Financial Situation: Evaluate your monthly expenses and how much income replacement you would require in the event of a disability.

- Employer Benefits: Check if your employer offers disability insurance as part of your benefits package. If so, understand the coverage limits and consider supplementing it with additional coverage if needed.

- Health and Risk Profile: Assess your overall health and lifestyle factors that might increase your risk of disability. This can help you determine the level of coverage necessary.

- Duration of Coverage: Depending on your age and career stage, consider how long you’ll need disability insurance. Younger individuals may want longer-term coverage to protect their income for decades to come.

In summary, disability insurance is a crucial safety net that prevents financial hardship when you can’t work due to disability. Understanding the types of disability insurance – short-term and long-term – empowers you to make informed decisions about the coverage that best suits your needs and circumstances. Don’t underestimate the importance of this protection; it could be a lifeline during challenging times.

2. The Importance of Disability Coverage

When it comes to securing your financial future, disability insurance stands as a pillar of protection. Let’s delve into why you need disability insurance and the dire financial consequences you might face without it.

2-1. Why Do You Need Disability Insurance?

Life is unpredictable, and an unexpected accident or illness can strike at any time, rendering you unable to work. In such a scenario, disability insurance serves as a lifeline. Here’s why it’s crucial:

2-1-1. Safeguarding Your Income

Disability insurance guarantees a portion of your income even when you can’t work. This means you can continue to pay your bills, cover daily expenses, and maintain your lifestyle. Without this safety net, you’d face significant financial challenges.

2-1-2. Peace of Mind for Your Loved Ones

Your financial responsibilities don’t vanish when you’re unable to work. Disability insurance eases the burden on your loved ones by ensuring they don’t have to shoulder the entire financial load during your disability.

2-1-3. Long-Term Financial Security

Disability insurance isn’t just about getting through the immediate challenges. It offers long-term financial security by preventing the depletion of your savings and investments, allowing you to focus on recovery without worrying about your financial stability.

2-2. Financial Consequences of Disability

Now, let’s explore the stark financial realities you might confront if you don’t have disability insurance in place:

2-2-1. Depleting Your Savings

Without disability coverage, you’d likely have to dip into your savings to make ends meet during your disability. Over time, this can erode your hard-earned financial cushion, leaving you vulnerable.

2-2-2. Accumulating Debt

To cover essential expenses, you might resort to accumulating debt, whether through credit cards, loans, or borrowing from friends and family. This can lead to a cycle of debt that’s challenging to break free from.

2-2-3. Struggling with Daily Expenses

Imagine facing disability-related medical bills, mortgage or rent payments, utilities, and groceries without a reliable source of income. It can quickly become overwhelming, leading to financial turmoil.

2-2-4. Risking Your Financial Future

The financial consequences of disability can extend far beyond the immediate crisis. You might jeopardize your long-term financial goals, such as saving for retirement, your children’s education, or buying a home.

2-2-5. Impact on Your Credit Score

Constantly relying on credit to cover expenses can harm your credit score. A lower credit score can impact your ability to secure loans or mortgages in the future, affecting your financial flexibility.

In summary, disability insurance is not a luxury but a necessity. It safeguards your income, provides peace of mind to your loved ones, and ensures your long-term financial security. Without it, the consequences can be severe, including depleting savings, accumulating debt, and risking your financial future. Investing in disability insurance is a wise step toward protecting your financial well-being in an unpredictable world.

3. Deciding Whether You Need Coverage

Disability insurance is a critical consideration for financial security in today’s uncertain world. Life’s unpredictability means that at any moment, you could face illness or injury that prevents you from working. Disability insurance serves as a vital safety net during these challenging times.

3-1. The Employer Factor

In many cases, sizable employers extend disability insurance benefits to their employees. Unfortunately, those working for smaller companies or self-employed individuals often find themselves without this crucial coverage. Being devoid of disability insurance can be a risky proposition, especially if your livelihood heavily depends on your employment income.

3-2. Marital and Financial Considerations

If you’re married and your spouse earns a substantial income, providing a safety net that can support your financial needs without your earnings might seem reasonable. Similarly, if you’ve amassed a significant financial cushion for your future, you may contemplate forgoing disability coverage. However, keep in mind that unforeseen circumstances might elevate your expenses, such as specialized care in case of disability.

3-3. The Unpredictable Nature of Disabilities

For most individuals, dismissing the necessity of disability coverage appears straightforward. The odds of enduring a prolonged disability may seem remote – and indeed, they are. Nevertheless, life can throw curveballs, and disability coverage can alleviate you, and possibly your family, from a substantial financial burden.

3-4. Types of Disabilities

It’s essential to acknowledge that most disabilities arise from medical conditions such as arthritis, heart ailments, hypertension, or impairments affecting the back, spine, hips, or legs. Surprisingly, over one-third of all disabilities afflict individuals under the age of 45. The vast majority of these medical issues cannot be foreseen, especially those resulting from random accidents.

3-5. Government Programs

You may believe that government programs offer adequate disability coverage. However, it’s crucial to reconsider this assumption:

3-5-1. Social Security Disability

Social Security provides long-term benefits only if you’re incapable of engaging in substantial, gainful activity for over a year or if your disability is anticipated to result in death. These payments are meager, designed solely to cover basic, subsistence-level living expenses.

3-5-2. Workers’ Compensation

This system offers benefits if you’re injured on the job but provides no support for disabilities occurring away from the workplace. You need coverage that offers protection regardless of where and how you become disabled.

3-5-3. State Disability Programs

A few states have disability insurance programs, but their coverage is typically minimal. Additionally, they don’t provide good value due to the high cost relative to the limited coverage they offer, with benefits paid out over a relatively short timeframe.

In summary, disability insurance is essential for everyone. Regardless of your job or financial situation, disabilities can strike unexpectedly. While government programs like Social Security and Workers’ Compensation have limitations, private disability insurance offers comprehensive coverage to safeguard your income and ensure financial stability when you need it most. Don’t delay – securing disability insurance is a wise financial choice for a secure future.

4. How to Choose the Right Disability Insurance

Choosing the right disability insurance is a crucial decision that can significantly impact your financial well-being in times of need. In this section, we’ll explore the factors you should consider when selecting disability insurance and understand how it differs from social security benefits.

4-1. Factors to Consider When Choosing Disability Insurance

Selecting disability insurance isn’t a one-size-fits-all process. It requires careful consideration of several factors to ensure it aligns with your unique circumstances:

4-1-1. Coverage Duration

Begin by evaluating how long you need disability coverage. Short-term disability insurance typically covers shorter periods, whereas long-term disability insurance provides more extended protection. Your age, career stage, and financial goals can influence this choice.

4-1-2. Benefit Amount

Determine the amount of income replacement you require during a disability. It’s essential to strike a balance between ensuring your essential expenses are covered and keeping premiums affordable.

4-1-3. Waiting Period

The waiting period, often referred to as the elimination period, is the duration you must wait after becoming disabled before your benefits start. Shorter waiting periods mean quicker access to benefits but may come with higher premiums.

Think of the waiting period as the deductible for disability insurance – it’s the duration between the onset of your disability and the commencement of benefit payments. Similar to other types of insurance, selecting the highest deductible (i.e., the longest waiting period) your finances allow can significantly reduce your insurance costs and eliminate the hassle of claiming for short-term disabilities. Most policies offer a minimum waiting period of 30 days, while the maximum could extend to one to two years. Opt for a waiting period of three to six months if you possess sufficient emergency reserves.

4-1-4. Definition of Disability

Review the policy’s definition of disability carefully. Some policies consider you disabled if you can’t perform your current job, while others may require you to be unable to perform any job.

The type of disability policy you choose is crucial. An own-occupation disability policy provides benefits if you cannot perform your regular job. Some policies only pay out if you are incapable of performing any job for which you are reasonably qualified. Own-occupation policies tend to be more expensive because they increase the likelihood of a payout. The extra cost may be justifiable if you are in a high-income or specialized occupation and switching careers would mean a substantial pay cut – a situation likely to affect your lifestyle adversely.

4-1-5. Noncancelable and Guaranteed Renewable

These policy features ensure that your coverage remains intact even if your health deteriorates. Some policies necessitate periodic physical examinations, which could jeopardize your coverage precisely when you need it most.

4-1-6. Cost of Premiums

Consider your budget and the cost of premiums. While disability insurance is essential, it should also be affordable. You may be able to adjust your benefit amount or waiting period to find a premium that fits your budget.

4-1-7. Additional Riders

Explore optional riders that can enhance your disability insurance policy. These riders may include features like cost-of-living adjustments, which help your benefits keep pace with inflation.

- Residual Benefits: This option provides partial benefits if your disability prevents you from working full-time, a valuable feature for those experiencing partial incapacitation.

- Cost-of-Living Adjustments (COLAs): COLAs automatically increase your benefit payment by a predetermined percentage each year or in line with inflation changes. This feature maintains the purchasing power of your benefits, making even a modest COLA, such as 3 to 4 percent, worth considering.

- Future Insurability: Some agents may suggest purchasing a future insurability clause, which allows you to acquire additional coverage regardless of your health. For most individuals, paying for this privilege is unnecessary if your current income accurately reflects your long-term earnings and spending expectations. However, if your present income is artificially low, but you anticipate substantial future growth (e.g., you are a recent medical school graduate in a low-paying residency), future insurability might be beneficial.v

4-1-8. Insurer’s Financial Stability

While insurer stability is vital, don’t become overly fixated on it. Benefits are typically paid out even if an insurer fails, as the state or another insurance entity often steps in to cover the claims.

4-2. Disability Insurance vs. Social Security

Understanding the differences between disability insurance and social security benefits is crucial, as they can complement each other:

4-2-1. Eligibility

Disability insurance is typically available through private insurance companies or employer-sponsored plans. Eligibility and benefits depend on the specific policy terms. Social security benefits, on the other hand, are government programs available to eligible individuals, including those who have paid into the system through payroll taxes.

4-2-2. Benefit Amount

The benefit amount in disability insurance is often based on your income and the policy’s terms, allowing for more customized coverage. Social security benefits are calculated using a formula that considers your average lifetime earnings.

4-2-3. Waiting Period

Disability insurance policies offer various waiting periods that you can choose based on your needs. Social security benefits usually have a more extended waiting period before benefits begin.

4-2-4. Flexibility

With disability insurance, you have more control over the coverage and can tailor it to your specific requirements. Social security benefits follow a standardized formula.

4-2-5. Possibility of Dual Coverage

It’s possible to have both disability insurance and social security benefits simultaneously. In fact, many financial advisors recommend having both to ensure comprehensive coverage in case of disability.

In conclusion, choosing the right disability insurance involves considering factors like coverage duration, benefit amount, waiting periods, and more. It’s a tailored approach to safeguarding your financial future. Additionally, understanding the distinctions between disability insurance and social security benefits can help you make informed decisions about your overall disability coverage strategy. Be sure to carefully review policy details, consult with insurance professionals, and select the disability insurance that best suits your needs.

5. How Much Disability Insurance You Need?

Determining the right amount of disability insurance is a critical step in securing your financial future. It ensures you can maintain your lifestyle if a disability unexpectedly strikes. In this section, we’ll explore key factors to consider when calculating the coverage you need.

5-1. Calculating the Right Coverage

The first step in obtaining disability insurance is determining the necessary coverage to sustain your quality of life until alternative financial resources become accessible. If you haven’t accumulated significant financial assets and wish to maintain your current lifestyle if a disability strikes seek coverage that replaces your entire monthly take-home pay after taxes.

5-2. Understanding Benefit Amounts

Disability insurance policies express benefits as the monthly sum you would receive if disabled. Therefore, if your job yields a $4,000-per-month income after taxes, aim for a policy that offers a $4,000-per-month benefit.

5-3. Tax Implications

Whether you pay for your disability insurance affects the taxability of benefits. Privately paid premiums yield tax-free benefits, although one hopes never to need them. In contrast, if your employer sponsors the coverage, the benefits are taxable, necessitating a larger benefit amount.

5-4. Duration of Coverage

It’s essential to select a policy that extends benefits until you reach an age when you can attain financial self-sufficiency. For most individuals, this occurs around ages 65 to 67, coinciding with the commencement of Social Security benefits. If you anticipate requiring employment income beyond your mid-60s, explore disability coverage that extends to a later age.

5-5. Short-Term Policies

If your calculations indicate that you are within five to ten years of financial independence or retirement, consider shorter-term disability policies. Such policies are also viable if you have confidence that someone, like a family member, can financially support you over the long term.

In conclusion, the amount of disability insurance you require depends on factors like your current income, tax implications, and the duration of coverage needed. To sustain your quality of life in the event of a disability, aim for coverage that replaces your after-tax income. Keep in mind that shorter-term policies may be suitable if you’re nearing financial independence or retirement. Ultimately, selecting the right disability insurance is about safeguarding your financial well-being and peace of mind.

6. Where to Buy Disability Insurance?

Deciding where to purchase disability insurance is a crucial financial decision. This article will help you navigate the options available to you and make an informed choice about where to secure this essential coverage.

6-1. Employer or Professional Association: Your Best Bet

The most cost-effective avenue to acquire disability insurance is often through your employer or a professional association. These group plans typically offer better value compared to individual policies. However, there are some important considerations to keep in mind.

6-1-1. Group Plans: Better Value with Caveats

Group plans can be a great choice, but they come with specific criteria, including benefit limits and qualification terms. Before you commit, make sure the group policy meets your needs and expectations.

6-1-2. Caution When Dealing with Agents

When it comes to choosing a disability insurance plan, it’s essential to exercise caution when relying on insurance agents for guidance. Why? Because agents may have a conflict of interest. They earn no commissions from group policy transactions, which could influence their recommendations.

6-2. When Group Plans Aren’t an Option

If you don’t have access to a group policy through your employer or professional association, you still have options.

6-2-1. Consulting Your Agent

One option is to consult your insurance agent, especially if you have a trusted relationship. However, proceed with caution. Some agents may try to add unnecessary features to your policy to boost their commissions. Make sure you clearly communicate your needs and budget to avoid overpaying for coverage you don’t need.

6-2-2. Trusted Insurance Providers

Another avenue is to explore trusted insurance providers independently. Research reputable companies, compare quotes, and read reviews to ensure you’re getting the best deal without unnecessary add-ons.

In conclusion, when deciding where to buy disability insurance, your best bet is often through your employer or a professional association. Group plans can provide excellent value, but it’s essential to understand their limitations. If a group plan isn’t available to you, consulting your agent or exploring reputable insurance providers can help you secure the coverage you need. Just remember to tread carefully, ensuring your policy aligns with your needs and doesn’t include unnecessary features that inflate costs. Making an informed choice will provide peace of mind and financial security in case you ever need to rely on your disability insurance.

7. The Cost of Disability Insurance

Understanding the cost of disability insurance is crucial for making informed decisions about this essential coverage. In this section, we’ll delve into how insurance companies calculate premiums and explore affordable disability insurance options.

7-1. How Premiums Are Calculated

Insurance premiums are the regular payments you make to maintain your disability insurance coverage. The calculation of these premiums involves several factors:

7-1-1. Your Age and Health

Younger individuals typically pay lower premiums for disability insurance. This is because they are considered lower risk for disability at a younger age. Your health also plays a role, as pre-existing medical conditions may lead to higher premiums.

7-1-2. Occupation and Risk Level

Your occupation can influence your premium. Jobs with higher physical demands or more significant safety risks may result in higher premiums because of the increased likelihood of disability claims.

7-1-3. Benefit Amount and Waiting Period

The amount of income replacement you choose and the waiting period before benefits kick in can impact your premiums. Higher benefit amounts and shorter waiting periods often lead to higher premiums.

7-1-4. Coverage Duration

The length of your disability insurance coverage, whether short-term or long-term, can affect your premiums. Long-term coverage is generally more expensive due to the extended protection it offers.

7-1-5. Optional Riders

Adding optional riders to your policy, such as cost-of-living adjustments or additional coverage, can increase your premiums. However, these riders can provide valuable benefits.

7-2. Affordable Disability Insurance Options

While disability insurance is essential, it’s also essential to find ways to make it more affordable without compromising on coverage. Here are some strategies:

7-2-1. Group Coverage

If your employer offers group disability insurance, take advantage of it. Group policies often have lower premiums and may even cover a portion of the cost.

7-2-2. Benefit Amount Adjustment

Consider adjusting the benefit amount to a level that meets your essential financial needs without overextending your budget. This can help lower your premiums.

7-2-3. Lengthen Waiting Period

Choosing a longer waiting period before benefits begin can reduce your premiums. However, be sure you can handle the financial implications of a longer waiting period.

7-2-4. Health and Lifestyle Improvements

Maintaining a healthy lifestyle and addressing pre-existing health conditions can potentially lead to lower premiums. Insurance companies may offer discounts for non-smokers and individuals with excellent health.

7-2-5. Shop Around

Compare disability insurance quotes from multiple providers to find the most competitive rates. Different insurers may offer varying premiums for the same coverage.

7-2-6. Eliminate Unnecessary Riders

While optional riders can enhance your coverage, they can also increase your premiums. Evaluate whether you truly need these riders and consider removing any that aren’t essential.

7-2-7. Payment Frequency

Paying your premiums annually instead of monthly can sometimes result in cost savings, as some insurers offer discounts for annual payments.

In summary, understanding how insurance companies calculate disability insurance premiums is vital in determining the cost of coverage. By considering factors like age, occupation, benefit amount, waiting period, and optional riders, you can make informed choices about your policy. Additionally, exploring affordable options such as group coverage, benefit adjustments, and lifestyle improvements can help you secure the protection you need without straining your budget. Don’t overlook the importance of disability insurance, and take proactive steps to make it a manageable and cost-effective part of your financial plan.

8. Filing a Disability Insurance Claim

Filing a disability insurance claim is a critical step in accessing the financial support you need when you can’t work due to disability. In this section, we’ll walk you through the claims process and highlight common mistakes to avoid to ensure a smooth and hassle-free experience.

8-1. The Claims Process

Understanding the steps involved in filing a disability insurance claim can help you navigate the process effectively:

8-1-1. Notify Your Insurance Company

As soon as you become disabled and anticipate needing to file a claim, notify your insurance company promptly. They will provide you with the necessary forms and guidance on how to proceed.

8-1-2. Complete Claim Forms

You’ll need to complete claim forms provided by your insurer. These forms typically require detailed information about your disability, medical history, and work-related details. Ensure accuracy and completeness when filling them out.

8-1-3. Medical Documentation

Gather all relevant medical documentation, including doctor’s reports, test results, and treatment plans. Your insurer will require this evidence to assess the validity of your claim.

8-1-4. Authorization to Obtain Records

Sign any necessary authorization forms that allow your insurer to obtain your medical records directly from healthcare providers. This expedites the claims review process.

8-1-5. Review by Claims Adjuster

Your insurance company will assign a claims adjuster to evaluate your disability claim. They may conduct interviews, review medical records, and assess your eligibility based on the policy terms.

8-1-6. Benefit Payment Determination

Once your claim is approved, the insurer will determine the benefit amount and payment schedule. Be sure to review the details to understand how much you’ll receive and when.

8-1-7. Ongoing Communication

Maintain open communication with your insurer throughout the claims process. Keep them informed of any changes in your condition or treatment to ensure your benefits are up to date.

8-2. Common Mistakes to Avoid

Avoiding common mistakes is crucial to prevent delays or denials of your disability insurance claim:

8-2-1. Delayed Notification

Failing to notify your insurance company promptly can result in delays in processing your claim. Notify them as soon as you anticipate needing to file a claim.

8-2-2. Incomplete or Inaccurate Forms

Incomplete or inaccurate claim forms can slow down the review process. Double-check all information to ensure it’s correct and comprehensive.

8-2-3. Missing Medical Documentation

Failure to provide necessary medical documentation can lead to claim denials. Ensure you gather all relevant records to support your claim.

8-2-4. Lack of Authorization

If you don’t sign authorization forms for the release of medical records, your insurer may struggle to obtain essential information, potentially delaying your claim.

8-2-5. Inconsistent Communication

Keep your insurer informed about any changes in your condition or treatment. Inconsistent communication can lead to misunderstandings and claim disputes.

8-2-6. Failure to Review Policy Terms

Understand the terms of your disability insurance policy, including waiting periods, benefit amounts, and coverage limits. Failing to do so may result in unrealistic expectations.

8-2-7. Missing Deadlines

Adhere to all deadlines set by your insurer, whether for claim submission or providing requested documentation. Missing deadlines can jeopardize your claim.

In conclusion, filing a disability insurance claim involves a series of essential steps, from notifying your insurer to gathering medical documentation and maintaining ongoing communication. Understanding and avoiding common mistakes can help ensure a smoother and more successful claims process. Remember that disability insurance is designed to provide financial support during challenging times, so taking these steps diligently is crucial to accessing the benefits you deserve.

9. Disability Insurance Myths Debunked

Navigating the world of disability insurance can be daunting, especially when common misconceptions cloud the truth. In this section, we’ll debunk some of the most prevalent myths about disability insurance and provide you with the facts you need to make informed decisions.

9-1. Common Misconceptions

9-1-1. Myth 1: “I’m Young and Healthy, I Don’t Need Disability Insurance”

- Reality: Disability can strike at any age. In fact, young adults are more likely to experience disability due to accidents or injuries. Disability insurance is essential for safeguarding your financial future, regardless of your age or health.

9-1-2. Myth 2: “I Have Savings, I’ll Be Fine Without Disability Insurance”

- Reality: While savings are important, they may not be sufficient to cover the expenses associated with a long-term disability. Disability insurance provides a steady income stream, ensuring you can maintain your lifestyle without depleting your savings.

9-1-3. Myth 3: “I Can Rely on Workers’ Compensation or Social Security”

- Reality: Workers’ compensation only covers work-related injuries or illnesses, and Social Security disability benefits are notoriously difficult to qualify for. Disability insurance offers more comprehensive coverage, including non-work-related disabilities.

9-1-4. Myth 4: “Disability Insurance is Too Expensive”

- Reality: The cost of disability insurance can be surprisingly affordable, especially when considering the financial security it provides. Many insurers offer options to tailor coverage to your budget, making it accessible for many individuals.

9-1-5. Myth 5: “I Have Health Insurance, So I’m Covered”

- Reality: Health insurance covers medical expenses but does not replace your lost income during a disability. Disability insurance complements your health coverage by ensuring your financial stability.

9-2. The Truth About Disability Insurance

9-2-1. Fact 1: Disability Insurance Protects Your Income

- Disability insurance provides income replacement when you’re unable to work due to disability. It ensures you can continue to meet financial obligations like mortgage or rent payments, utility bills, and daily expenses.

9-2-2. Fact 2: It Covers a Wide Range of Disabilities

- Disability insurance isn’t limited to workplace injuries. It covers various disabilities, including those caused by accidents, illnesses, and chronic conditions, offering comprehensive protection.

9-2-3. Fact 3: Customizable Coverage

- Disability insurance policies are flexible and can be tailored to your needs. You can adjust benefit amounts, waiting periods, and other features to align with your unique circumstances and budget.

9-2-4. Fact 4: It’s Essential for Your Financial Security

- Your ability to earn an income is one of your most valuable assets. Disability insurance safeguards your financial future by preventing the depletion of savings and investments when you can’t work.

9-2-5. Fact 5: Peace of Mind for Your Loved Ones

- Disability insurance doesn’t just benefit you; it provides peace of mind to your loved ones, knowing they won’t be burdened with your financial responsibilities during your disability.

In summary, debunking common myths about disability insurance is essential to understanding its true value. Disability can affect anyone, and relying on misconceptions can leave you vulnerable. The reality is that disability insurance is a vital asset that protects your income, covers various disabilities, offers customizable coverage, and ensures your financial security. Don’t let myths hold you back from securing the protection you and your family need.v

10. Conclusion

In conclusion, disability insurance provides peace of mind in uncertain times. It’s a financial lifeline that can prevent you from facing dire consequences if disability strikes. So, is disability insurance worth it? Absolutely. It’s a prudent investment in your financial security.

11. FAQs

11-1. What is disability insurance, and how does it work?

Disability insurance is a financial safeguard that provides you with income replacement if you become disabled and cannot work due to injury or illness. It ensures you receive regular payments, typically a percentage of your salary, to help you maintain your standard of living and cover essential expenses when you can’t earn a paycheck.

11-2. What are the main types of disability insurance?

There are two primary types of disability insurance: short-term disability (STD) and long-term disability (LTD) coverage. STD insurance provides benefits for a limited duration, ideal for temporary disabilities. LTD insurance offers more extended protection for severe and long-lasting disabilities, like chronic illnesses.

11-3. Why do I need disability insurance if I have savings or health insurance?

While savings and health insurance are crucial, they may not be enough to cover the expenses associated with a disability. Disability insurance provides steady income replacement, ensuring you can meet financial obligations without depleting your savings or relying solely on health coverage.

11-4. How do I choose the right disability insurance policy?

Choosing the right disability insurance involves considering factors such as coverage duration, benefit amount, waiting periods, and your financial situation. It’s essential to tailor your policy to your specific needs, assess your employer benefits, and understand your health and risk profile.

11-5. Can I have both disability insurance and social security benefits?

Yes, it’s possible and often recommended to have both disability insurance and social security benefits. Disability insurance offers customizable coverage, while social security benefits depend on specific government programs. Having both ensures comprehensive protection in case of disability, covering various scenarios and income levels.

12. Case Study

Michael is a 37-year-old male architect with a deep passion for design, art, and travel. He’s happily married with two adorable children, and their family unit is his utmost priority.

Michael’s stable income of $90,000 per year from his architecture job has allowed them to comfortably cover their monthly expenses, which amount to approximately $6,000.

Their financial portfolio includes savings of $50,000, investments worth $30,000, and they own a home valued at $300,000. However, they are still paying off a mortgage of $200,000 and have a car loan of $15,000.

12-1. Current Situation

Michael is a successful architect who is passionate about his work and providing for his family. He enjoys traveling and spending quality time with his wife and two young children. With a stable income of $90,000 per year, he has been able to comfortably cover their monthly expenses of $6,000. Life seems good until an unexpected event unfolds.

12-2. Conflict Occurs

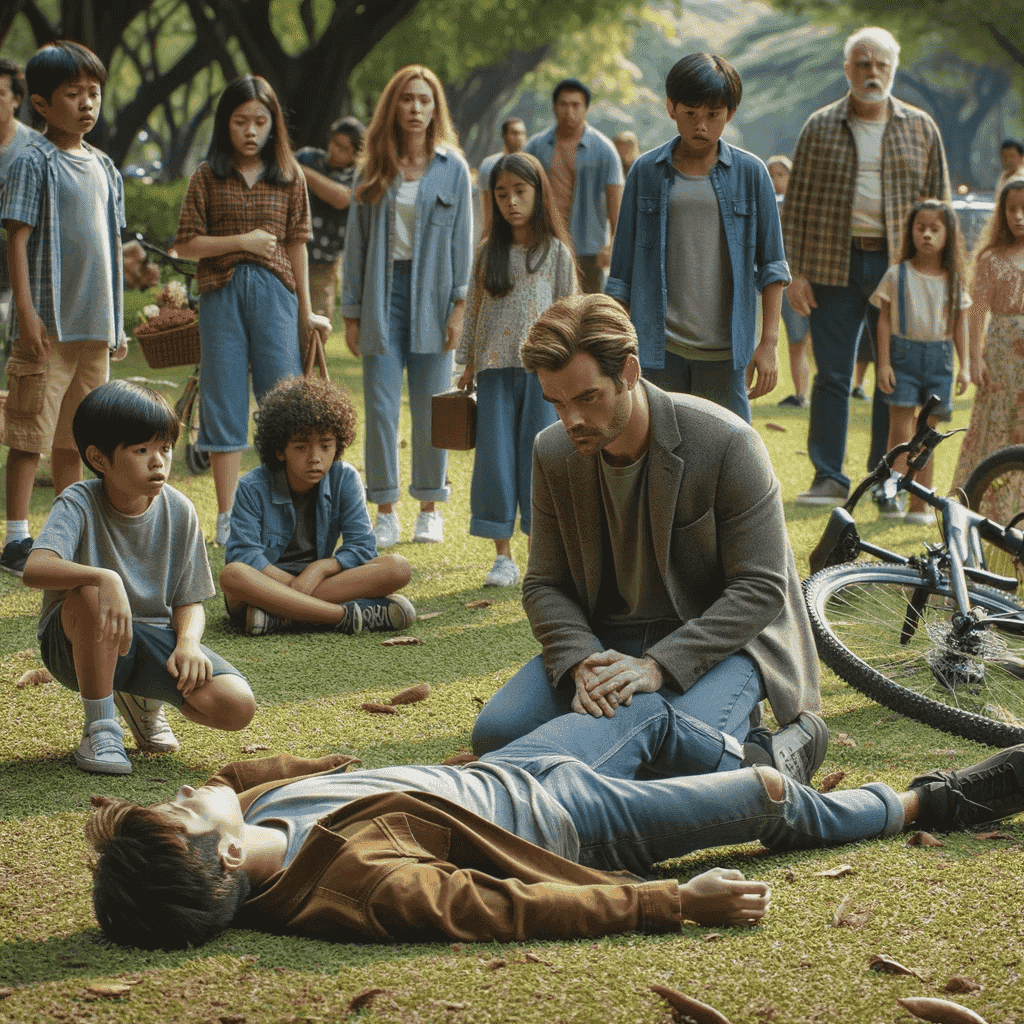

One sunny afternoon, while his friend Mark joins him for a cycling trip in the park with Michael’s kids, Mark suffers a severe accident, resulting in a fractured leg and multiple injuries. Mark is immediately rushed to the hospital and undergoes surgery. The doctor delivers the shocking news: he won’t be able to work for at least six months.

Witnessing Mark’s predicament, Michael is filled with a mix of emotions—fear, concern, and empathy for his friend. He also realizes that if a similar accident were to happen to him, his family’s financial stability would be at risk. This experience inspires him to reevaluate his financial preparedness and consider disability insurance.

12-3. Problem Analysis

The incident with Mark opens Michael’s eyes to the potential financial vulnerability his family faces in the event of his own disability. He recognizes the dilemma: without an income replacement plan, he and his family would struggle to meet monthly expenses, including the mortgage, car loan, and daily necessities. This crisis could jeopardize their financial well-being.

12-4. Solution

After witnessing Mark’s situation and discussing it with his spouse, Michael decides to invest in disability insurance. He understands that disability insurance is a vital safety net to protect his income and his family’s future. He selects a policy with a monthly premium of $150, providing a benefit of $7,500 per month in case of disability. The policy has a waiting period of 30 days and offers coverage until age 65.

The implementation involves completing the application, understanding the waiting period, and ensuring the policy provides long-term coverage. Michael overcomes initial concerns about the cost of premiums by adjusting the benefit amount and waiting period to fit his budget.

12-5. Effect After Execution

Once the disability insurance policy is in place, it takes effect immediately. Although Michael has to pay monthly premiums of $150, he gains peace of mind knowing that his family’s financial security is protected. In case of another unexpected disability, they won’t face the same financial crisis that Mark is going through.

The positive effects of this decision are immense. Michael’s family can maintain their lifestyle and meet financial obligations even during his recovery period. His biggest feeling after overcoming this problem is relief and gratitude for having taken proactive steps to secure their future.

12-6. In Conclusion

Michael’s story emphasizes the importance of disability insurance in safeguarding one’s financial well-being. Witnessing his friend’s accident served as a wake-up call, inspiring him to assess his own financial vulnerabilities and take action. His advice to others facing similar situations is to evaluate their financial preparedness, consider disability insurance, and make informed decisions to protect their income and family’s future. In the end, Michael found that disability insurance was indeed worth it in ensuring his family’s financial stability during challenging times.

13. Checklist

| Questions | Your Reflection | Recommended Improvement Strategies | Improvement Plan | Implementation Results | Review and Adjust |

| 1. Do I understand what disability insurance is? | Explore articles or resources to gain a better understanding of disability insurance. | ||||

| 2. Have I assessed my financial situation? | Review my monthly expenses and evaluate how much income replacement I would need in the event of a disability. | ||||

| 3. Am I aware of my employer’s disability benefits? | Contact HR or the benefits department to understand the coverage limits and consider supplementing it if necessary. | ||||

| 4. Have I considered my health and risk profile? | Evaluate my overall health and lifestyle factors that might increase my risk of disability to determine the level of coverage necessary. | ||||

| 5. Do I know the different types of disability insurance? | Research and learn about short-term and long-term disability insurance to determine which aligns with my needs. | ||||

| 6. Have I calculated the right amount of coverage? | Calculate the necessary coverage based on my monthly take-home pay and consider tax implications. | ||||

| 7. Am I familiar with how premiums are calculated? | Understand how age, health, occupation, benefit amount, waiting period, and optional riders can impact premium costs. |