First-time car insurance, often referred to as “new driver” or “teen driver” insurance, is essential for young adults as they enter the world of driving. This specialized auto insurance addresses the unique needs of inexperienced drivers, ensuring their safety and financial security on the road. In this guide, we’ll delve into the fundamentals of first-time car insurance, its significance, coverage options, and practical tips for finding affordable policies.

Reading time: 25 minutes

Outline

1. Understanding the Basics of First Time Car Insurance

First-time car insurance, also known as “new driver” or “teen driver” insurance, is a specialized type of auto insurance designed specifically for young adults who are either obtaining their driver’s licenses or purchasing their first vehicles. This coverage is tailored to the unique needs and circumstances of young, inexperienced drivers, and it plays a crucial role in ensuring their safety and financial well-being on the road.

1-1. What Is First Time Car Insurance?

First-time car insurance is essentially a lifeline for young adults who are taking their first steps into the world of driving. It provides a safety net that shields them from the potential financial consequences of accidents or damages that may occur while they are behind the wheel.

1-1-1. Customized Coverage for Novice Drivers

One of the key features of first-time car insurance is its customization to meet the specific requirements of inexperienced drivers. Insurance providers recognize that young adults have a higher likelihood of being involved in accidents due to their limited driving experience. Therefore, policies are tailored to address this risk, ensuring that young drivers have adequate protection.

1-1-2. Comprehensive Protection

First-time car insurance typically offers comprehensive coverage, encompassing various aspects of auto insurance. This includes liability coverage, which protects young drivers from potential legal and financial liabilities if they are deemed responsible for an accident. Additionally, it often includes collision coverage, which covers the costs of repairing or replacing the insured vehicle in the event of a collision, regardless of fault.

1-1-3. Affordable Premiums

While young adults might expect their insurance premiums to be sky-high due to their age and inexperience, many insurance companies offer affordable options for first-time car insurance. This is achieved through various discounts and tailored pricing structures that take into account factors like good grades, driver education courses, and safe driving habits.

1-2. Why Is It Important for Young Adults?

First-time car insurance is not just a mere legal requirement imposed by most states; it’s a vital tool for ensuring the financial security and peace of mind of young adults as they embark on their driving journey.

1-2-1. Legal Compliance

In the United States, most states mandate that all drivers, regardless of age, must have some form of auto insurance. For young adults, first-time car insurance is their ticket to legal compliance, allowing them to enjoy the freedom and independence that comes with driving.

1-2-2. Financial Protection

Accidents are unpredictable and can happen to anyone at any time. For young adults without insurance, the aftermath of an accident could lead to substantial expenses that may be difficult to bear. First-time car insurance serves as a financial safety net, covering medical bills, vehicle repairs, and other associated costs, sparing young drivers and their families from the burden of these expenses.

1-2-3. Safeguarding Future Assets

Beyond immediate financial protection, first-time car insurance also safeguards the long-term financial well-being of young adults. If a young driver is found liable for an accident, they could face significant legal claims and lawsuits. Without insurance, this could jeopardize their future assets and earnings. With insurance, they have a shield that protects their financial future.

Ideally, your coverage should be at least double your assets. Even if you are just starting to accumulate assets, don’t assume you don’t need liability protection. Many states have minimum requirements, and your future earnings can be at risk in a lawsuit. Property damage liability insurance, which covers damage to other people’s property or cars caused by your vehicle, is typically determined based on your bodily injury liability coverage. Starting with coverage of $50,000 is advisable.

In conclusion, first-time car insurance is a vital tool for young adults stepping into the world of driving. It offers tailored coverage, affordability, legal compliance, and most importantly, peace of mind. For young adults, it’s not just an expense; it’s an investment in their safety and financial security on the road.

2. How to Find Affordable First Time Car Insurance

Finding affordable first-time car insurance is a priority for young adults, but it’s not just about price—it’s about securing the right coverage that fits your unique needs and budget. To make an informed decision, you need to understand the factors that affect first-time car insurance rates and employ effective strategies for comparing quotes.

2-1. Factors That Affect First Time Car Insurance Rates

When insurers calculate your first-time car insurance rates, they take various factors into account. Understanding these factors can help you grasp why your rates may differ from others and how to potentially lower them.

2-1-1. Age

Age plays a significant role in determining your insurance premium. Young adults typically have higher rates because they have less driving experience, which makes them more prone to accidents. As you gain more experience and establish a clean driving record, your rates may decrease over time.

2-1-2. Location

Where you live can impact your insurance rates as well. Urban areas often have higher rates due to increased traffic congestion and a higher likelihood of accidents. Conversely, rural areas tend to have lower rates because of less traffic and lower accident risks.

2-1-3. Vehicle Type

The type of vehicle you drive also influences your insurance rates. Sports cars and luxury vehicles typically come with higher premiums due to their higher repair and replacement costs. Choosing a safe and practical vehicle can help reduce your insurance costs.

2-1-4. Driving History

Your driving history is a critical factor. A clean record with no accidents or traffic violations can lead to lower premiums. Conversely, a history of accidents or citations can result in higher rates.

2-1-5. Coverage Options

The coverage options you choose impact your premium. More comprehensive coverage, such as lower deductibles and additional coverage like rental car reimbursement, will increase your rates. Consider your needs and budget carefully when selecting coverage options.

2-2. Tips for Comparing Quotes

Now that you understand the factors affecting your insurance rates, let’s explore effective strategies for comparing quotes and finding the most affordable first-time car insurance.

2-2-1. Obtain Multiple Quotes

Don’t settle for the first quote you receive. Shop around and obtain quotes from several insurance providers. This allows you to compare rates, coverage options, and discounts to find the best fit.

2-2-2. Look for Discounts

Insurance providers offer various discounts that can significantly reduce your premium. Some common discounts include good student discounts, safe driver discounts, and discounts for completing driver education courses. Be sure to inquire about these opportunities.

2-2-3. Bundle Policies

Consider bundling your first-time car insurance with other policies, such as renters or homeowners insurance, with the same provider. Bundling often results in a substantial discount on all policies.

2-2-4. Adjust Coverage

Evaluate your coverage needs carefully. While comprehensive coverage is essential, you may be able to adjust certain elements, such as deductibles, to lower your premium without sacrificing essential protection.

2-2-5. Explore Different Deductibles

The deductible is the amount you pay out of pocket in the event of a claim. Choosing a higher deductible can lower your premium but also means you’ll pay more in case of an accident. Determine the deductible that aligns with your financial comfort level.

2-2-6. Consider Usage-Based Insurance

Some insurance providers offer usage-based insurance programs that track your driving habits using telematics devices. If you’re a safe driver, this can result in lower rates based on your actual driving behavior.

2-3. Buying Auto Insurance

To obtain auto insurance quotes, you can follow the same process as when buying homeowner’s or renter’s insurance. You can use the resources provided by your homeowner’s insurer or explore options from organizations like AAA/Auto Club and Progressive. Comparing quotes from multiple sources can help you find the best coverage at the most competitive rates.

In conclusion, finding affordable first-time car insurance requires a combination of understanding the factors that influence your rates and employing effective strategies for comparing quotes. By taking the time to shop around, look for discounts, and adjust your coverage options, you can secure the right insurance coverage that fits your needs and budget, providing you with peace of mind as you hit the road. Remember, informed decisions lead to better outcomes when it comes to your first-time car insurance.

3. Coverage Options Explained

When selecting your first-time car insurance policy, it’s crucial to understand the various coverage options available to ensure you have the right protection for your needs. Let’s delve into the details of these coverage options, including liability coverage, collision coverage, and comprehensive coverage.

3-1. Liability Coverage

Liability coverage is a fundamental component of first-time car insurance policies, and it’s mandatory in most states. This coverage serves as a safety net in case you’re involved in an accident where you’re at fault, and it’s designed to protect both you and other parties affected by the accident.

3-1-1. Protecting Others

The primary purpose of liability coverage is to cover the costs associated with injuries or property damage caused to other parties involved in an accident you’re responsible for. This can include medical expenses, vehicle repairs, and legal fees if you’re sued.

3-1-2. Minimum Coverage Requirements

Each state has specific minimum liability coverage requirements that you must meet to legally drive. These requirements vary from state to state, so it’s essential to know your state’s minimums and ensure your policy complies.

3-2. Collision Coverage

Collision coverage is another crucial component of first-time car insurance, and it provides protection for your own vehicle in the event of an accident, regardless of fault. This coverage helps cover the cost of repairing or replacing your car when it’s damaged in a collision.

3-2-1. Own Vehicle Protection

Collision coverage is designed to safeguard your investment in your vehicle. Whether you collide with another car, a stationary object, or even if your vehicle rolls over, this coverage steps in to help you get back on the road without bearing the full financial burden of repairs.

3-2-2. Deductibles

When you choose collision coverage, you’ll also select a deductible, which is the amount you’ll pay out of pocket before your insurance kicks in. A higher deductible can lower your premium but means you’ll be responsible for more of the repair costs in case of an accident.

3-3. Comprehensive Coverage

Comprehensive coverage offers protection against a wide range of non-collision-related incidents that can damage or harm your vehicle. It’s often referred to as “other than collision” coverage and is especially valuable for safeguarding your car from theft, vandalism, and natural disasters.

3-3-1. Protection Beyond Collisions

Comprehensive coverage extends your insurance protection beyond typical accidents. It covers scenarios such as theft, fire damage, vandalism, hailstorms, falling objects (like tree branches), and even animal collisions. This coverage ensures that you’re covered in various unexpected situations.

3-3-2. Deductibles and Premiums

Similar to collision coverage, comprehensive coverage comes with a deductible. You can adjust the deductible amount to balance your premium cost and out-of-pocket expenses. Keep in mind that comprehensive coverage may be required if you have a car loan or lease.

3-4. Uninsured or Underinsured Motorist Liability

In the unfortunate event of an accident with an uninsured or underinsured motorist, this coverage allows you to collect for lost wages, medical expenses, and pain and suffering. While it may seem redundant if you already have comprehensive health and long-term disability insurance, dropping this coverage means giving up the ability to sue for general pain and suffering and to protect passengers without adequate coverage. To provide financial support for dependents in case of a fatal auto accident, consider purchasing term life insurance.

In conclusion, navigating the world of first-time car insurance is less daunting when you have a clear understanding of the available coverage options. From liability coverage to comprehensive coverage, each serves a unique purpose in safeguarding you on the road. By tailoring your policy to your specific needs, you can drive with confidence, knowing you’re adequately protected. Don’t forget to consider uninsured or underinsured motorist liability and, for added peace of mind, think about term life insurance to protect your loved ones in case of the unexpected. Your journey on the road can be a secure and worry-free one with the right coverage in place.

4. Navigating the Claims Process

Understanding how to navigate the claims process effectively is essential in the unfortunate event of a car accident. When you have first-time car insurance, knowing the steps to follow after an accident and being aware of common mistakes to avoid can make a significant difference in the outcome of your insurance claim.

4-1. Steps to Follow After an Accident

4-1-1. Ensuring Safety First

The safety of all parties involved should be your immediate concern. After an accident, safely move your vehicle to the side of the road, if possible, to prevent further collisions. Turn on your hazard lights to alert other drivers, and check if anyone is injured. If there are injuries, call 911 immediately for medical assistance.

4-1-2. Gather Essential Information

Once safety is ensured, gather crucial information for your insurance claim. Exchange contact information, insurance details, and driver’s license information with all parties involved in the accident. Take photos of the accident scene, including vehicle damage, license plates, and any relevant road signs or conditions. This documentation will be invaluable during the claims process.

4-1-3. Notify Law Enforcement

Depending on the severity of the accident, you may need to report it to the police. Many insurance companies require a police report for certain claims. Even if it’s not mandatory, having an official record of the accident can be beneficial when filing your claim.

4-1-4. Contact Your Insurance Company

After ensuring everyone’s safety and gathering essential information, contact your insurance company promptly. The sooner you report the accident, the sooner they can begin processing your claim. Provide them with all the details and documentation you’ve collected.

4-1-5. Follow Medical Advice

If you or anyone else is injured, seek medical attention immediately. Follow the advice of healthcare professionals and keep records of your medical treatment. Medical records can be essential when claiming compensation for injuries.

4-1-6. Cooperate with the Claims Adjuster

Your insurance company will assign a claims adjuster to your case. Cooperate fully with them, providing all requested information and documentation. The adjuster will assess the damage, review your policy, and guide you through the claims process.

4-2. Common Mistakes to Avoid

4-2-1. Admitting Fault

One common mistake to avoid after an accident is admitting fault. Even if you believe you may have contributed to the accident, it’s crucial not to admit fault at the scene. Determining fault is the job of insurance companies and, if necessary, the legal system. Admitting fault can complicate your claim and affect your coverage.

4-2-2. Neglecting to Report Promptly

Another critical mistake is delaying the reporting of the accident to your insurance company. Timely reporting is essential because some policies have specific time limits for filing claims. Failing to report promptly may result in your claim being denied.

4-2-3. Providing Incomplete Information

When reporting the accident to your insurance company, be thorough and provide complete information. Leaving out details or providing inaccurate information can delay the claims process and affect the outcome of your claim.

4-2-4. Not Documenting the Accident

Failing to document the accident scene can be a significant mistake. Without photos and other evidence, it becomes challenging to prove your case or assess the extent of the damage. Always document the accident to the best of your ability.

4-2-5. Accepting a Settlement Too Quickly

Avoid accepting a settlement from the other party’s insurance company too quickly, especially if you have sustained injuries. Consult with your own insurance company and legal counsel before making any decisions.

In conclusion, knowing how to navigate the claims process is crucial when you have first-time car insurance. Following the correct steps after an accident, gathering essential information, and avoiding common mistakes can help ensure a smoother and more successful claims experience. Remember that your insurance company is there to assist you, so be diligent and cooperative throughout the process to secure the coverage you deserve.

5. Building a Safe Driving Record

Building a safe driving record is not only essential for your safety on the road but also plays a significant role in reducing your first-time car insurance premiums. In this section, we’ll delve into the details of how you can establish a safe driving record and its impact on your insurance costs.

5-1. Defensive Driving Tips

The high number of annual road fatalities in the United States emphasizes the importance of safe driving. While tragic events often dominate headlines, auto accidents claim the lives of more than 30,000 people each year. Many of these accidents are preventable. Practicing safe driving habits, staying within speed limits, avoiding driving under the influence, and wearing seat belts can significantly reduce the risk of accidents.

5-1-1. Avoiding Distractions

One of the most crucial aspects of safe driving is avoiding distractions. Keep your focus on the road, and never use your phone while driving. Texting, making calls, or even changing the music on your device can divert your attention and lead to accidents.

5-1-2. Obeying Traffic Rules

Strictly adhering to traffic rules is another key component of defensive driving. This includes obeying speed limits, stopping at stop signs, yielding the right of way, and using turn signals. Following these rules not only keeps you safe but also helps prevent accidents caused by violations.

5-1-3. Maintaining a Safe Following Distance

Maintaining a safe following distance from the vehicle in front of you is essential. This gives you ample time to react if the vehicle ahead suddenly stops or encounters an obstacle. The recommended following distance is at least three seconds.

5-1-4. 5-1-1. Being Cautious in Adverse Weather

Weather conditions can significantly affect road safety. When driving in adverse weather such as rain, snow, or fog, reduce your speed and increase your following distance. Ensure your vehicle’s lights are on, and use caution on slippery roads.

5-1-5. Handling Road Rage

Avoid engaging in road rage or aggressive driving behavior. Stay calm, and if you encounter an aggressive driver, do not escalate the situation. Instead, try to move away from them safely.

5-2. The Impact of Good Driving Habits

5-2-1. Lower Insurance Premiums

Good driving habits have a direct impact on your insurance premiums. Insurance providers often reward safe drivers with discounts and lower rates. Maintaining a clean driving record, free from accidents and traffic violations, demonstrates to insurers that you are a responsible and low-risk driver.

5-2-2. Safe Driver Discounts

Many insurance companies offer safe driver discounts to policyholders with a history of safe driving. These discounts can significantly reduce your insurance costs over time, making it financially beneficial to drive responsibly.

5-2-3. Long-Term Savings

Building a safe driving record is not just about the immediate benefits; it’s a long-term investment. As you accumulate years of safe driving experience, you can enjoy lower insurance rates for an extended period, resulting in substantial savings over the life of your first-time car insurance policy.

5-2-4. Enhanced Safety

Beyond the financial benefits, good driving habits promote enhanced safety on the road for both you and other drivers. Being a responsible driver contributes to a safer driving environment for everyone.

In conclusion, building a safe driving record is a win-win situation. It not only ensures your safety and the safety of others on the road but also leads to significant financial benefits in the form of lower first-time car insurance premiums. By following defensive driving tips and consistently practicing good driving habits, you can establish a strong track record of responsible driving that will benefit you for years to come. Remember, safe driving isn’t just a choice; it’s an investment in your safety and financial well-being.

6. Discounts and Savings Opportunities

Navigating the world of first-time car insurance can be a complex task, but it’s essential to explore discounts and savings opportunities to make the most of your coverage. In this section, we’ll uncover strategies to reduce your insurance costs, such as student discounts, bundling policies, and other smart ways to save.

6-1. Student Discounts

6-1-1. Good Grades Pay Off

One of the most common discounts available for young adults is the student discount. Many insurance providers offer this discount to students who maintain good grades in school. The rationale behind this discount is that students who excel academically tend to exhibit responsible behavior, which extends to their driving habits.

6-1-2. Eligibility Criteria

To qualify for a student discount, you typically need to meet certain criteria, such as:

- Full-time enrollment in high school or college

- A minimum grade point average (GPA) requirement, often a B average or higher

- Proof of your academic achievements, such as a report card or transcript

It’s essential to check with your insurance provider for their specific eligibility criteria, as they may vary from one company to another.

6-1-3. Potential Savings

Student discounts can lead to significant savings on your first-time car insurance premiums. The exact amount of the discount varies, but it’s not uncommon to see reductions of 10% or more on your annual premium. Over time, these savings can add up, making it financially advantageous to maintain strong academic performance.

6-2. Bundling Policies for Savings

6-2-1. What Is Bundling?

Bundling policies is another effective way to save money on your first-time car insurance. This strategy involves purchasing multiple insurance policies from the same insurance provider. Typically, this includes bundling your car insurance with other policies such as renters or homeowners insurance.

6-2-2. Benefits of Bundling

Bundling policies offer several benefits:

- Discounts: Insurance companies often offer substantial discounts to customers who bundle their policies. These discounts can result in significant cost savings on your insurance premiums.

- Convenience: Managing your insurance policies becomes more convenient when they are all with the same provider. You’ll have a single point of contact for all your insurance needs.

- Streamlined Claims: In the event of a claim that involves multiple policies, having all your policies with one provider can simplify the claims process.

6-2-3. Factors to Consider

While bundling policies can be advantageous, it’s essential to consider a few factors:

- Policy Compatibility: Ensure that the insurance provider offers the coverage and policy types that meet your needs. Not all providers offer all types of insurance.

- Cost and Coverage: Compare the overall cost and coverage options when bundling policies to ensure you’re getting a good deal. Sometimes, it may be more cost-effective to purchase policies separately if they provide better coverage.

- Cancellation Policies: Understand the provider’s cancellation policies in case you need to make changes to your policies in the future.

6-3. Deductibles

Choosing higher deductibles can help reduce your auto insurance premiums and eliminate the need to file small claims. Most people can comfortably consider a deductible in the range of $500 to $1,000. Auto policies have two types of deductibles:

- Collision deductible applies to claims resulting from collisions.

- Comprehensive deductible covers damages not caused by collisions, such as vandalism or broken windows.

As your car depreciates in value, you can eventually eliminate comprehensive and collision coverage. The decision on when to do this depends on your personal circumstances and risk tolerance.

6-4. Special Discounts

Explore potential discounts on your auto insurance policy. Inform your agent or insurer about security features in your car, such as alarms, airbags, or anti-lock brakes. Additionally, being older or having multiple policies or vehicles with the same insurer might qualify you for discounts. Ensure that you receive “good driver” discounts if you have a clean driving record.

When considering a new vehicle purchase, obtain insurance quotes for different models beforehand, as insurance costs can significantly impact your ongoing expenses.

6-5. Skip Little-Stuff Coverage

Auto insurers offer various optional riders, such as towing and rental car reimbursement. While these may seem affordable, they often provide minimal benefits relative to the hassle of filing a claim. Similarly, riders who waive deductibles under specific circumstances may not make practical sense, as the purpose of deductibles is to reduce policy costs and eliminate minor claims.

6-6. Medical Payments Coverage

Evaluate whether medical payment coverage is necessary for you. This coverage typically pays only a few thousand dollars for medical expenses. If you and your passengers already have substantial medical insurance coverage, this rider may not be essential. Additionally, a few thousand dollars may not suffice for catastrophic medical expenses.

In conclusion, maximizing discounts and savings in your first-time car insurance policy is a smart financial move. Whether it’s through good student discounts, bundling policies, adjusting deductibles, or exploring special discounts, you can make your insurance more cost-effective without compromising on coverage. Remember that informed decisions can lead to significant savings in the long run, allowing you to enjoy the benefits of affordable and reliable auto insurance coverage.

7. Conclusion

First-time car insurance is not just a requirement; it’s a crucial investment in the safety and financial stability of young adults as they begin their driving journey. By grasping the basics, exploring coverage choices, and employing cost-saving strategies, you can make informed decisions that lead to cost-effective and dependable insurance coverage. Remember that responsible driving and a clean record can further bolster your financial well-being. So, as you embark on your driving adventure, ensure you have the right coverage to safeguard yourself, your vehicle, and your peace of mind.

8. FAQs

8-1. What is first-time car insurance, and why is it important for young adults?

First-time car insurance is specialized auto coverage designed for young adults who are new to driving. It’s crucial because it provides financial protection in case of accidents, ensuring the safety and financial security of inexperienced drivers.

8-2. What does first-time car insurance typically cover?

First-time car insurance usually offers comprehensive coverage, including liability coverage for accidents you may cause, collision coverage for your vehicle, and sometimes, even protection against non-collision incidents like theft or vandalism.

8-3. How can I find affordable first-time car insurance rates?

To find affordable rates, consider factors like your age, location, vehicle type, and driving history. Compare quotes from multiple providers, look for discounts such as good student discounts, and consider bundling policies to save money.

8-4. What should I do if I get into an accident with my first-time car insurance?

After an accident, ensure safety first, gather essential information and contact your insurance company promptly. Avoid admitting fault, report the accident as soon as possible, and cooperate with your claims adjuster.

8-5. How can I build a safe driving record to lower my first-time car insurance premiums?

Building a safe driving record involves following defensive driving tips, obeying traffic rules, and avoiding distractions. Safe driving habits can lead to discounts, lower premiums, and enhanced safety on the road.

9. Case Study

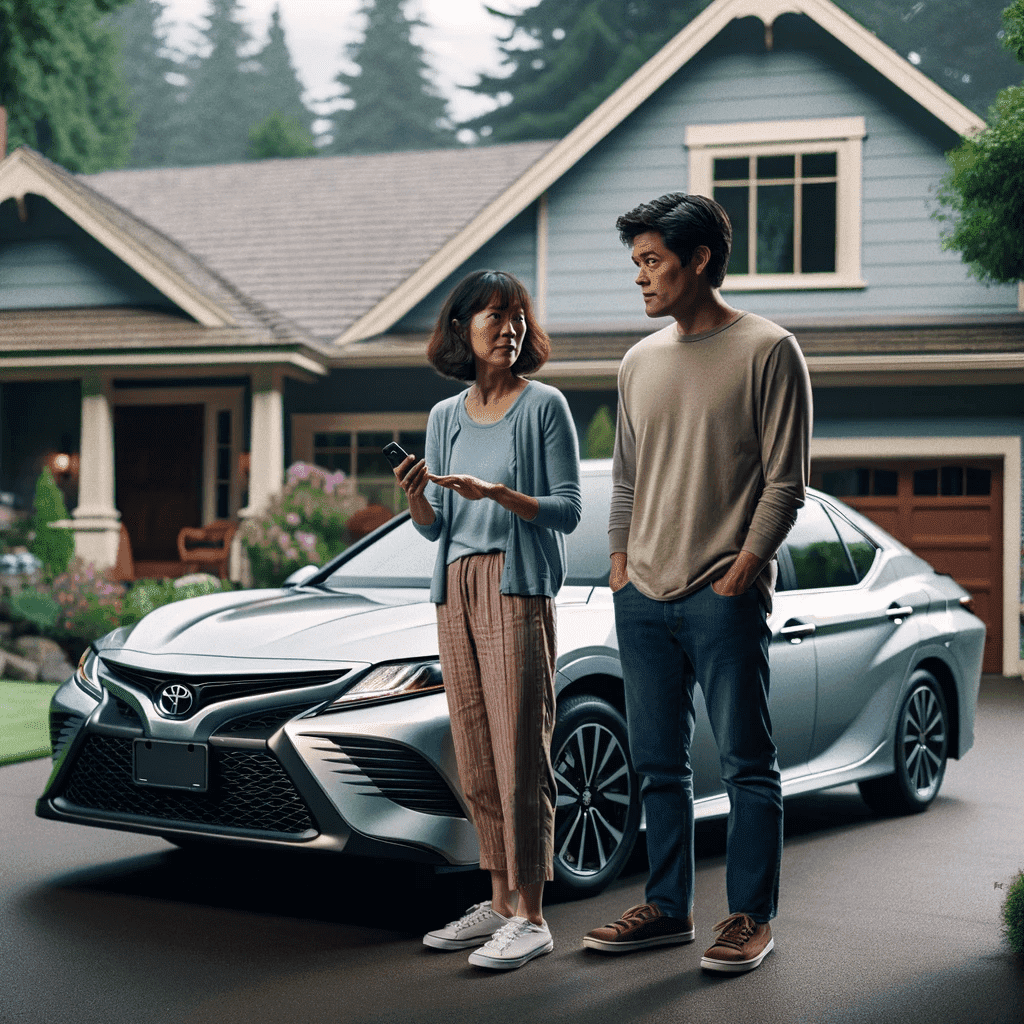

James, a 45-year-old male software developer with a keen interest in technology and cars, is married to Susan, who is 43 years old. Together, they have a teenage son named Michael, who is 17 years old.

James earns an annual income of $80,000 while managing monthly household expenses of approximately $4,000. Their assets include homeownership valued at $250,000, a savings account with $20,000, and a family car worth $15,000. However, they also have a mortgage balance of $150,000 with monthly payments of $1,200.

9-1. Current Situation

James is a 45-year-old software developer with a wife, Susan, and a teenage son, Michael. Michael recently obtained his driver’s license and is eager to start driving the family car. James and Susan own a family car, a 2019 Toyota Camry valued at $15,000, which their son will be using. As a responsible parent, James needs to ensure that his son has proper insurance coverage as a first-time driver to guarantee his safety on the road and protect the family financially in case of any accidents.

9-2. Conflict Occurs

James encounters difficulties when he realizes that insuring a first-time driver can be costly. Given their moderate income and the need to manage monthly household expenses of approximately $4,000, he feels a mix of emotions, including concern for his son’s safety, the stress of managing the family budget, and the responsibility of finding affordable first-time car insurance. Despite the financial strain, he understands the importance of securing proper coverage for his son and protecting their family’s financial well-being.

9-3. Problem Analysis

The dilemma arises from the high insurance rates associated with first-time drivers, especially teenagers. James’s annual income of $80,000 supports their household, which includes mortgage payments of $1,200 per month. With Michael now driving, the family faces an additional expense they need to accommodate. James is concerned about the potential impact on their monthly budget and savings goals. If the issue is not resolved, the family could face increased expenses, putting a strain on their finances and potentially impacting their ability to meet other financial goals, such as saving for Michael’s college education.

9-4. Solution

James decides to research affordable first-time car insurance options while keeping their budget and financial goals in mind. He explores different insurance providers and policies, looking for discounts that can help mitigate the high premiums associated with young drivers. To maximize savings, he considers factors like good student discounts, safe driver courses, and bundling car insurance with their existing policies.

After careful consideration, James chose an insurance policy with a premium of $2,500 per year. The policy provides comprehensive coverage, including liability, collision, and comprehensive coverage, with a $1,000 deductible. To reduce costs, James encourages his son, Michael, to maintain good grades and enroll in a safe driver education course to qualify for additional discounts. They decide to bundle their car insurance with their existing homeowner’s insurance, which results in an additional annual discount of $500.

9-5. Effect After Execution

The solution begins to take effect within a few weeks. The total annual insurance cost for the family amounts to $2,000 after factoring in discounts. While the insurance premium remains relatively high due to the first-time driver status, the discounts help reduce the overall cost. James and Susan feel relieved knowing that their son is adequately covered, and they have taken steps to manage the associated expenses.

The cost of implementing the solution is $2,000 annually, which they consider a manageable expense given their income and budget. The positive effect is a sense of security for the family, knowing they have prioritized their son’s safety on the road. James realizes the importance of balancing safety with costs when it comes to first-time car insurance for young drivers.

9-6. In Conclusion

James, a software developer and a responsible parent, faced the dilemma of securing affordable first-time car insurance for his teenage son, Michael. With an annual income of $80,000 and monthly household expenses of $4,000, James chose a solution that balanced cost and coverage, ensuring his son’s safety and financial protection on the road. The positive effect is a sense of security for the family, and his advice to others facing similar challenges is to research discounts and consider bundling policies to make first-time car insurance more affordable while considering their budget and financial goals.

10. Checklist

| Questions for Self-Reflection | Your Reflection | Recommended Improvement Strategies | Improvement Plan | Implementation Results | Review and Adjust |

| Have I obtained first-time car insurance coverage? | If not, research insurance options for young adults and consider obtaining coverage. | ||||

| Do I understand the key coverage options available in first-time car insurance? | Review the article to better grasp liability, collision, and comprehensive coverage. | ||||

| Am I aware of the factors affecting first-time car insurance rates? | Revisit the article and take note of age, location, driving history, and vehicle type factors. | ||||

| Have I explored strategies to find affordable first-time car insurance rates? | Implement the tips mentioned in the article, such as comparing quotes and seeking discounts. | ||||

| Do I know the steps to follow after an accident with first-time car insurance? | Familiarize myself with the accident response process outlined in the article. | ||||

| Am I aware of common mistakes to avoid when dealing with first-time car insurance claims? | Study the article’s insights on avoiding mistakes like admitting fault and reporting promptly. | ||||

| Have I considered building a safe driving record to lower my first-time car insurance premiums? | Apply defensive driving tips and obey traffic rules as suggested in the article. |